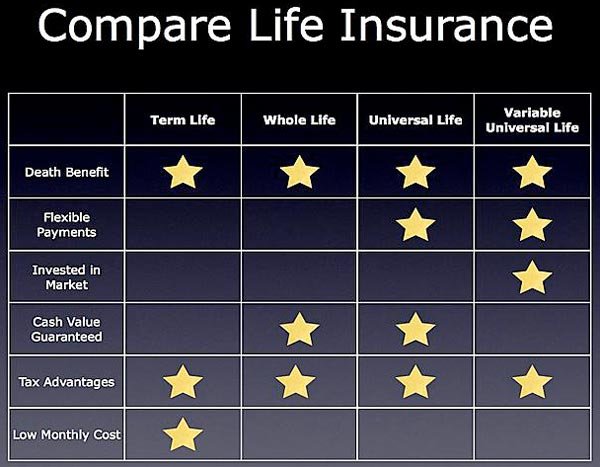

Variable Life Insurance

Permanent life insurance is a term for life insurance plans that, unlike term life insurance, doesn’t expire and by combining a death benefit with a savings portion, can build a cash value. The policy owner can borrow funds against this cash value, and in some instances, they can withdraw the cash value to help meet future goals such as paying a child’s college tuition.

However, there is usually a waiting period after the purchase of your policy if you want to borrow against the savings portion of permanent life insurance. This is because a certain period of time has to pass in order for sufficient cash value to accumulate.

However, there is usually a waiting period after the purchase of your policy if you want to borrow against the savings portion of permanent life insurance. This is because a certain period of time has to pass in order for sufficient cash value to accumulate.

These life insurance policies also have favorable tax treatment. This means you don’t pay any taxes on any earnings in the policy as long as your policy stays active. If you stick to certain premium limits, you can take money out of the policy without being subjected to taxes. As long as you don’t exceed the number of premiums paid when you’re withdrawing funds, you won’t be taxed.

Variable Life Insurance Policy

Variable Life Insurance Policy

A variable life insurance policy is a type of permanent life insurance. It enables permanent protection to the beneficiary after the death of the policyholder. This type of insurance is often more expensive than term life insurance. It allows the insured person to transfer a portion of the premium dollars to a different account that consists of various instruments and investments inside the insurance company’s portfolio. These can be in the form of equity funds, money market funds, stocks, bonds, and bond funds.

However, just like with any other investment, there are risks. That’s why variable policies are regulated under the federal security laws as they are considered as securities contracts. As such, fund performance may lead to the decline of cash value or death benefit over time.

When it comes to tax benefits that were made available a to policy holders of variable life insurance, they have the ability to apply cash value on a tax-benefited basis. As long as they pay the premiums and the policy remains in force, the policy holder can access the cash value through a tax-free loan. However, if the cash value isn’t borrowed but instead withdrawn, the policyholder will face tax implications on any realized earnings. If a loan that’s taken out isn’t repaid in due time, the death benefit paid to the beneficiaries, which gets paid after the insured person passes away, will most likely decrease.

Variable Life Insurance Flexibility

A thing that makes variable life insurance different from permanent life insurance policies is the flexibility it provides to the policyholder in terms of premiums paid and cash value growth. Here, the premiums paid to traditional life insurance policies are not fixed. They can increase or decrease within certain limits over time, all based on the insurer’s needs. For example, if a person who has a variable life insurance policy decides that they want to reduce the monthly premium payment because they have an expense that they can’t cover without reducing the payments, they can do it.

The shortage in the premium payments can be covered by the cash value within the policy. And when the cash flow has returned to normal, the policy user can continue paying the initial fee of the payments.

Downsides of Variable Life Insurance

Just like with any other good thing, variable life insurance has its downsides. Unlike fixed life insurance, variable life insurance may require the policyholders to, over time, add premiums to make sure the death benefit stays guaranteed to a certain age. If you pay more than the minimum cost of insurance for this type of insurance policy (which is usually around $100) you will probably insure that the guarantees remain intact.

Just like with any other good thing, variable life insurance has its downsides. Unlike fixed life insurance, variable life insurance may require the policyholders to, over time, add premiums to make sure the death benefit stays guaranteed to a certain age. If you pay more than the minimum cost of insurance for this type of insurance policy (which is usually around $100) you will probably insure that the guarantees remain intact.

Another thing to be aware of is that the investment risks within the cash value of this type of insurance falls completely on the policyholder and not on the insurance company. This is why there are now guarantees to how well the cash value will perform over time, so it is practically impossible to plan how the money will be used in the future after it’s paid back to the beneficiary.

And just like with any other life insurance policy, if someone wants to take out a variable insurance policy, they need to undergo a full medical exam.

More in Motivation

-

`

Protein’s Role in Your Diet: Friend or Foe?

Protein’s Role in Your Diet: Friend or Foe?Protein, a word synonymous with muscle building and healthy living, has become a major focus in our food choices. From protein-infused...

March 8, 2024 -

`

5 Reasons Why Outdoor Personal Training Will Transform You

5 Reasons Why Outdoor Personal Training Will Transform YouIt’s that time of the year when spring whispers the promise of renewal, beckoning us to shed the winter blues and...

February 29, 2024 -

`

Atkins Diet: The Ultimate Solution for Weight Loss

Atkins Diet: The Ultimate Solution for Weight LossAre you ready to embark on a journey towards a healthier lifestyle? While the ketogenic diet has been hogging the spotlight...

February 22, 2024 -

`

ADHD Knows No Boundaries: Even Celebrities Are Affected

ADHD Knows No Boundaries: Even Celebrities Are AffectedAttention deficit hyperactivity disorder (ADHD) often conjures images of bouncing-off-the-walls children struggling to sit still in class. But what if we...

February 15, 2024 -

`

How to Navigate Medicare and Insurance Options in 2024

How to Navigate Medicare and Insurance Options in 2024As we age, maintaining good dental health becomes more important than ever. However, according to the Kaiser Family Foundation, nearly half...

February 6, 2024 -

`

How to Do HIIT on an Elliptical Machine? A Guide to Healthier Living

How to Do HIIT on an Elliptical Machine? A Guide to Healthier LivingAt the core of this fitness approach is the elliptical machine, also fondly known as the cross trainer. This gym staple...

February 3, 2024 -

`

10 Winter Smoothie Recipes to Savor the Season

10 Winter Smoothie Recipes to Savor the SeasonWinter’s chill might make you crave cozy soups, but let’s not forget the magic a blender can bring to your cold...

January 24, 2024 -

`

The Heart and Soul of ‘Percy Jackson’: Aryan Simhadri on Embodying Grover

The Heart and Soul of ‘Percy Jackson’: Aryan Simhadri on Embodying GroverImagine stepping into a world where ancient myths come alive, where your best friend isn’t just a regular teenager but a...

January 20, 2024 -

`

Everything You Need to Know About Grace Period in Health Insurance Plans

Everything You Need to Know About Grace Period in Health Insurance PlansImagine missing your health insurance premium payment by just a day and facing a health crisis the next day. Scary, right?...

January 10, 2024

More From TelehealthDave

-

Health InsuranceDoes Insurance Cover Physical Therapy?

Health InsuranceDoes Insurance Cover Physical Therapy?When it comes to physical therapy, a common question arises: Do you use health insurance for physical therapy? Well, navigating the...

July 25, 2024 -

FitnessDoes Coughing Work Your Abs? Here’s All You Ought to Know

FitnessDoes Coughing Work Your Abs? Here’s All You Ought to KnowWhen it comes to unexpected ways to engage your core, you might find yourself asking: Does coughing work your abs? The...

July 19, 2024 -

Nutrition & Weight LossHow to Prepare Rice Water for Weight Loss – Benefits and Uses

Nutrition & Weight LossHow to Prepare Rice Water for Weight Loss – Benefits and UsesRice water isn’t just a staple in traditional remedies—it’s a powerhouse of benefits for health and beauty. From treating diarrhea to...

July 12, 2024 -

MotivationAmanda Bynes Pregnant at 13? Debunking the Rumors

MotivationAmanda Bynes Pregnant at 13? Debunking the RumorsIn recent years, the internet has been ablaze with rumors surrounding former child star Amanda Bynes, particularly regarding allegations of a...

July 1, 2024 -

Health InsuranceCan Baking Soda Clean Your Lungs?

Health InsuranceCan Baking Soda Clean Your Lungs?Years of inhaling cigarette smoke, pollution, and other toxins can leave you longing for a way to cleanse your lungs. The...

June 27, 2024

You must be logged in to post a comment Login