Variable Life Insurance

Permanent life insurance is a term for life insurance plans that, unlike term life insurance, doesn’t expire and by combining a death benefit with a savings portion, can build a cash value. The policy owner can borrow funds against this cash value, and in some instances, they can withdraw the cash value to help meet future goals such as paying a child’s college tuition.

However, there is usually a waiting period after the purchase of your policy if you want to borrow against the savings portion of permanent life insurance. This is because a certain period of time has to pass in order for sufficient cash value to accumulate.

However, there is usually a waiting period after the purchase of your policy if you want to borrow against the savings portion of permanent life insurance. This is because a certain period of time has to pass in order for sufficient cash value to accumulate.

These life insurance policies also have favorable tax treatment. This means you don’t pay any taxes on any earnings in the policy as long as your policy stays active. If you stick to certain premium limits, you can take money out of the policy without being subjected to taxes. As long as you don’t exceed the number of premiums paid when you’re withdrawing funds, you won’t be taxed.

Variable Life Insurance Policy

Variable Life Insurance Policy

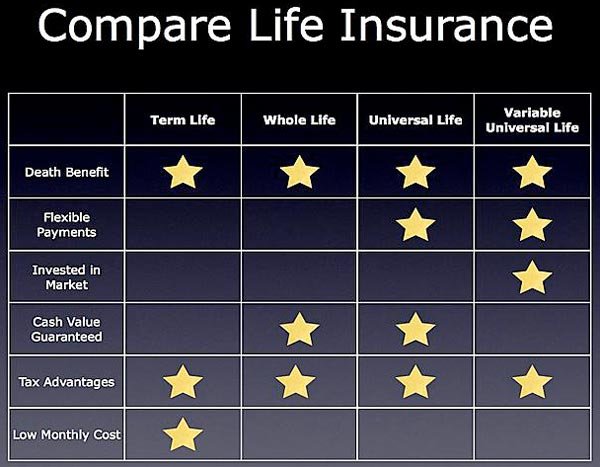

A variable life insurance policy is a type of permanent life insurance. It enables permanent protection to the beneficiary after the death of the policyholder. This type of insurance is often more expensive than term life insurance. It allows the insured person to transfer a portion of the premium dollars to a different account that consists of various instruments and investments inside the insurance company’s portfolio. These can be in the form of equity funds, money market funds, stocks, bonds, and bond funds.

However, just like with any other investment, there are risks. That’s why variable policies are regulated under the federal security laws as they are considered as securities contracts. As such, fund performance may lead to the decline of cash value or death benefit over time.

When it comes to tax benefits that were made available a to policy holders of variable life insurance, they have the ability to apply cash value on a tax-benefited basis. As long as they pay the premiums and the policy remains in force, the policy holder can access the cash value through a tax-free loan. However, if the cash value isn’t borrowed but instead withdrawn, the policyholder will face tax implications on any realized earnings. If a loan that’s taken out isn’t repaid in due time, the death benefit paid to the beneficiaries, which gets paid after the insured person passes away, will most likely decrease.

Variable Life Insurance Flexibility

A thing that makes variable life insurance different from permanent life insurance policies is the flexibility it provides to the policyholder in terms of premiums paid and cash value growth. Here, the premiums paid to traditional life insurance policies are not fixed. They can increase or decrease within certain limits over time, all based on the insurer’s needs. For example, if a person who has a variable life insurance policy decides that they want to reduce the monthly premium payment because they have an expense that they can’t cover without reducing the payments, they can do it.

The shortage in the premium payments can be covered by the cash value within the policy. And when the cash flow has returned to normal, the policy user can continue paying the initial fee of the payments.

Downsides of Variable Life Insurance

Just like with any other good thing, variable life insurance has its downsides. Unlike fixed life insurance, variable life insurance may require the policyholders to, over time, add premiums to make sure the death benefit stays guaranteed to a certain age. If you pay more than the minimum cost of insurance for this type of insurance policy (which is usually around $100) you will probably insure that the guarantees remain intact.

Just like with any other good thing, variable life insurance has its downsides. Unlike fixed life insurance, variable life insurance may require the policyholders to, over time, add premiums to make sure the death benefit stays guaranteed to a certain age. If you pay more than the minimum cost of insurance for this type of insurance policy (which is usually around $100) you will probably insure that the guarantees remain intact.

Another thing to be aware of is that the investment risks within the cash value of this type of insurance falls completely on the policyholder and not on the insurance company. This is why there are now guarantees to how well the cash value will perform over time, so it is practically impossible to plan how the money will be used in the future after it’s paid back to the beneficiary.

And just like with any other life insurance policy, if someone wants to take out a variable insurance policy, they need to undergo a full medical exam.

More in Motivation

-

`

5 ‘Bad’ Fitness TikTok Trends You Shouldn’t Follow

5 ‘Bad’ Fitness TikTok Trends You Shouldn’t FollowTikTok has become a haven for creative fitness advice. But not all trends are worth your time or your health. From...

November 23, 2024 -

`

Does Drinking Water Affect Adrenal Hormones?

Does Drinking Water Affect Adrenal Hormones?Drinking water is often seen as a simple way to stay hydrated, but it has deeper effects on our body than...

November 14, 2024 -

`

Why We Feel the Loss of Celebrities So Deeply?

Why We Feel the Loss of Celebrities So Deeply?Celebrity grief might sound strange at first. After all, most of us have never met these famous figures in person, yet...

November 5, 2024 -

`

Are High Deductible Insurance Plans as Ideal as They Appear to Be?

Are High Deductible Insurance Plans as Ideal as They Appear to Be?High deductible insurance plans have been a hot topic for years, especially as healthcare costs continue to rise. For many Americans,...

October 31, 2024 -

`

How Training Load Data Can Transform Your Exercise Routine

How Training Load Data Can Transform Your Exercise RoutineTracking progress during workouts is challenging. Simple metrics like mileage or time don’t show the whole picture. Understanding the overall effort...

October 26, 2024 -

`

Katy Perry’s Weight Loss Journey: Secret Diet Tips Revealed

Katy Perry’s Weight Loss Journey: Secret Diet Tips RevealedKaty Perry’s weight loss journey has been making headlines, with the pop star shedding 20 pounds over the past few months....

October 16, 2024 -

`

Celebrity Trainer Jeanette Jenkins Shares 5 Key Workout Motivations

Celebrity Trainer Jeanette Jenkins Shares 5 Key Workout MotivationsJeanette Jenkins is one of the most sought-after celebrity trainers, known for her ability to motivate and inspire people to achieve...

October 8, 2024 -

`

How to Spot Lung Problems Early and Protect Your Health

How to Spot Lung Problems Early and Protect Your HealthLung problems can sneak up on anyone, affecting breathing and overall well-being. Recognizing early symptoms can be crucial in preventing severe...

October 2, 2024 -

`

How to Get Into ‘Breaking Shape’ | A Guide for First-Timers

How to Get Into ‘Breaking Shape’ | A Guide for First-TimersBreaking is not just a dance style. It is a full-body workout. To get into breaking shape, you will need more...

September 27, 2024

More From TelehealthDave

-

Nutrition & Weight LossCan Kombucha Help You Lose Weight? Here’s What Research Says

Nutrition & Weight LossCan Kombucha Help You Lose Weight? Here’s What Research SaysKombucha has long been associated with various health benefits, from improved digestion to a boost in immunity. Recently, some researchers have...

April 17, 2025 -

MotivationSharon Osbourne on Her Weight Loss Struggles – “I Went Too Far”

MotivationSharon Osbourne on Her Weight Loss Struggles – “I Went Too Far”Sharon Osbourne has been open about her struggles with weight management over the years, trying everything from surgical procedures to diet...

April 8, 2025 -

Health InsuranceWhy People Are Choosing CrowdHealth Over Traditional Insurance

Health InsuranceWhy People Are Choosing CrowdHealth Over Traditional InsuranceHealth insurance has long been the backbone of medical coverage in the United States. However, with rising premiums, complex claims processes,...

April 2, 2025 -

FitnessWomen-Only Gym Faces Backlash Over Policy Change, Refunds Offered

FitnessWomen-Only Gym Faces Backlash Over Policy Change, Refunds OfferedNatalee Barnett, a well-known fitness influencer and gym owner, recently shared a major update about her upcoming gym, The Girls Spot,...

March 25, 2025 -

Nutrition & Weight LossHow the Liver’s Metabolism Affects Weight Loss – A New Study Explains

Nutrition & Weight LossHow the Liver’s Metabolism Affects Weight Loss – A New Study ExplainsMany people feel frustrated when weight loss slows after an initial period of success. Researchers may have found a way to...

March 20, 2025

You must be logged in to post a comment Login